Buying a Home in 2022: What You Need to Know

Table of content

In 2022, purchasing a property can be hectic and challenging. Prices have temporarily paused their rapid ascent, interest rates have spiked, and inventory is gradually growing. But sellers don’t want to lose out on what may be the latter stages of the seller’s market since buyers are still in a rush to acquire a house.

However, many house owners in Florida are reconsidering whether they even want to advertise their properties for sale in the Florida Real Estate market at this time. In addition to deciding whether they want to deal with a traditional real estate agent or attempt to save money by choosing a flat-fee real estate broker, they are determining if the uncertainty of a sale in the Florida Real Estate market is worth the amount of real estate commission they would pay. There isn’t a set of guidelines for this sort of market, and these are unpredictable times. You could still be able to purchase your ideal house in 2022, however, if you keep a few general trends and ideas in mind in the Florida Real Estate market.

Establish a Budget

Use an online mortgage affordability calculator to determine how much home you can afford before meeting with a mortgage provider. You may estimate how much money you should set aside for your down payment and closing fees after you know the price range in which you’ll be able to buy a property. Aim to save a minimum of $25,000 for your down payment and potentially an extra $7,000 to $10,000 for closing expenses, for instance, if an affordability calculator indicates that you are likely to be able to finance a $500,000 property.

Some various mortgage calculators calculate your monthly payment based on the cost of the house, the size of the down payment, the interest rate, the length of the loan, and other monthly mortgage costs like homeowner’s insurance, property taxes, and homeowners association dues. But keep in mind that this is only a guess. To find out how much you qualify for, you’ll need to get in touch with a mortgage lender. But in any case, you will have to accumulate the amount of the down payment and preferably several monthly mortgage payments, because if you do not have the money for this, then even if you use fit my money, it will be difficult for you to pay this amount even with loans.

Examine House Pricing in Advance

Due to strong demand from buyers and a limited number of available homes, home prices have increased this year. Those factors may not alter by 2022. It becomes sensitive to do a preliminary study on various communities to see which ones offer affordable housing costs. Before examining the figures, some purchasers start hunting for homes. However, it’s preferable to go in the other direction; first, choose where you can search, and then start driving out to visit various properties in person. Going the other way might result in you falling in love with a house or community that you can’t afford.

Get Ready for More Shock

Yes, you should prepare to be shocked—and not in a good way—if you’re planning to purchase a house in 2022. In many areas of the nation, if not almost everywhere, house prices have surpassed previous all-time highs at this stage in the cycle. Due to the low supply and high demand for homes, there is a substantial probability you will pay more for the property in question than the Zestimate or Redfin Estimate. These computerized values now seem to be adjusted upward every day and every week. The bad news for renters is that in 2022, property prices are predicted to increase, even more, meaning that costs are only going up.

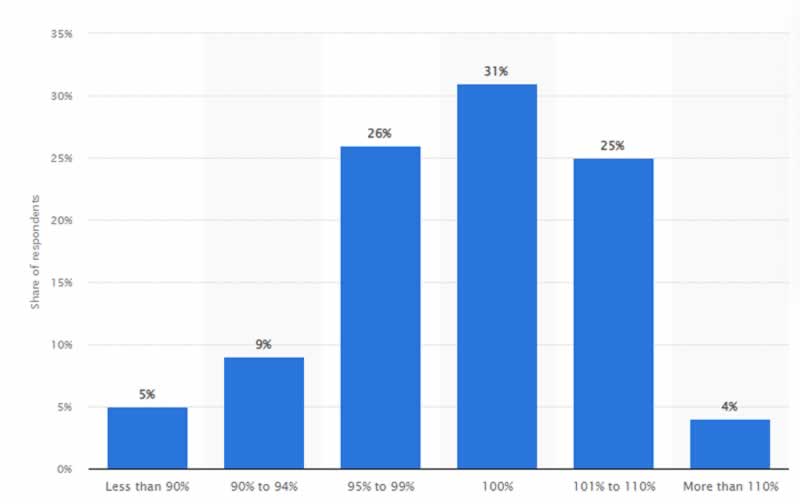

In other words, if you want a house next year, be prepared to spend a lot of money. Even if the asking price looks excessive, you could have to pay much more. In the United States, 31% of homebuyers in 2021 paid the full asking price for their property. On the other side, a total of 29% of property purchasers paid more than the asking price for their properties. Therefore, it is important to carefully study the offer to purchase and prepare for possible additional costs.

Check Your Credit

Your credit score affects both your mortgage rate and whether you are qualified for one. Your rate will decrease the better your score. The majority of mortgage programs need a credit score between 580 and 620. Before requesting a home loan, you should ideally verify your credit history at least six to twelve months in advance. This gives you time, if needed, to raise a bad credit score.

Look Around for Lenders and Get a Mortgage Pre-Approval

The kind of mortgage and lender both have different lending standards. For certain mortgages, the down payment required might be as little as 0%. Making a larger down payment, however, provides a few benefits: Because there is a decreased chance of default when a borrower contributes more to the acquisition, lenders could offer cheaper rates. Additionally, a large down payment may boost the likelihood that an offer will be approved by giving sellers assurance that your financing will be complete.

Don’t Forget Recession Fears and Future Housing Trends

When buying a property gets more and more out of reach, buyer competition declines, which might mean that inventory becomes available where you’re shopping. The number of houses that were up for sale nationwide in June increased by 18.7% from the same month last year. The likelihood that you will be able to purchase the house you want this year rather than scurrying in a bidding battle for whatever is available within your budget increases since there are more properties available to pick from.

There is, however, also concern about an impending recession. Instead of possibly spending too much for a property that would lose value in a future economic crisis, you might prevent this if you wait to purchase. Additionally, if the economy weakens, the Federal Reserve would likely increase interest rates gradually, which might be advantageous for prospective homebuyers looking to lock in a lower mortgage rate.

Is the Year 2022 a Bad Year to Buy a Home?

To be honest, there are advantages and disadvantages to purchasing a home in 2022. The fact that your interest rates will be among the lowest in history is positive. This is significant because it allows you to purchase a larger home and, in the case of a shorter mortgage, maybe pay it off more quickly since borrowing costs are so cheap (30-year mortgages are under 4%, while 15-year mortgages are around 3%). You will pay less in interest over the course of the loan as a result. The home-buying process has become more difficult and competitive, which is a drawback. Home prices have increased significantly compared to typical, and buyer bidding wars have caused some properties to sell for thousands of dollars more than they were originally listed for. Both motives to purchase and reasons to postpone a purchase will always exist.

Conclusion

Before touring properties, it’s critical to be aware of your absolute necessities, desirable features, and deal-breakers. Knowing what you can and cannot compromise on can help you decide whether to take advantage of an opportunity and when to pass it up. Another important factor is location. Investigate the areas and towns you’re considering to select a house you’ll adore for many years to come. Also, of course, use the tips and market trends that we told you about in this article.

About the author – John Barnes

Handyman tips website was created by John Barnes from Phoenix, Arizona, in February 2014. John wanted to share with the public his 20 year experience in home improvement as a contractor and avid woodworker. John noticed that there aren’t many expert advice online and he wanted to help the public to get true expert tips and estimates. What started as a hobby soon became a full time job as Handyman tips website became very popular because of the quality of tips it provides. After a few years John has introduces a couple of new content creators into Handyman tips team but he is still the main content creator on Handyman tips website.

Handyman tips website was created by John Barnes from Phoenix, Arizona, in February 2014. John wanted to share with the public his 20 year experience in home improvement as a contractor and avid woodworker. John noticed that there aren’t many expert advice online and he wanted to help the public to get true expert tips and estimates. What started as a hobby soon became a full time job as Handyman tips website became very popular because of the quality of tips it provides. After a few years John has introduces a couple of new content creators into Handyman tips team but he is still the main content creator on Handyman tips website.